As of last year, Houston’s tax increment reinvestment zones (TIRZs) had just under $1 billion in combined liabilities. The lion’s share of these liabilities is slightly over $80 million in bonds secured by the TIRZs, pledging their future property tax receipts. The balance of the liabilities is a potpourri of obligations, running from trade account payables to agreements to reimburse developers for improvements they have constructed.

To put the $800 million of bonds issued by the TIRZs in some perspective, as of last year, the City of Houston only had about twice that amount ($1.723 billion) outstanding for all of its public improvement bonds. In other words, the TIRZs have issued a third of the total amount of bonds the City has borrowed for public infrastructure work.1

Just three of the TIRZs (Uptown, Midtown, and Main Street) account for over half the TIRZ bond debt. The recent research from Baker Institute shows that the median income in these three TIRZs was at least 50% higher than the City’s median income.

The Uptown TIRZ alone accounts for 36% ($296 million) of the total bond debt. Included in that $296 million is $102 million issued by the Uptown TIRZ for affordable housing. According to its audit, City Council has, incredibly, already authorized the Uptown TIRZ to issue an additional $232 million in “affordable housing” bonds.

It is important to understand that the TIRZs' bonds are absolutely an obligation of the City of Houston and hence, its taxpayers. The only source of repayment of these bonds is future property tax receipts by the City, which will be transferred to the TIRZs so they can make the bond payments. Also, if any of the TIRZs are terminated, the City must assume their bond debt.

That means the TIRZs have tied up well over a billion dollars in future City property tax collections to service their bond debt. Those future property tax revenues will not be available to the City to pay for police, fire, garbage pickup, etc. It will take almost $400 million of future property tax receipts just to service the bond debt run up by the Uptown TIRZ.

The City Council approved all of this debt. If the City had issued these bonds directly, voter approval would have been required. This is because the legislature, in its infinite wisdom, decided that bonds issued by the TIRZs would not require voter approval, creating a loophole cities can drive a Mack truck through. Of course, City Council could ask for voter approval even though the statute does not require it. I am not going to hold my breath waiting for that to happen.

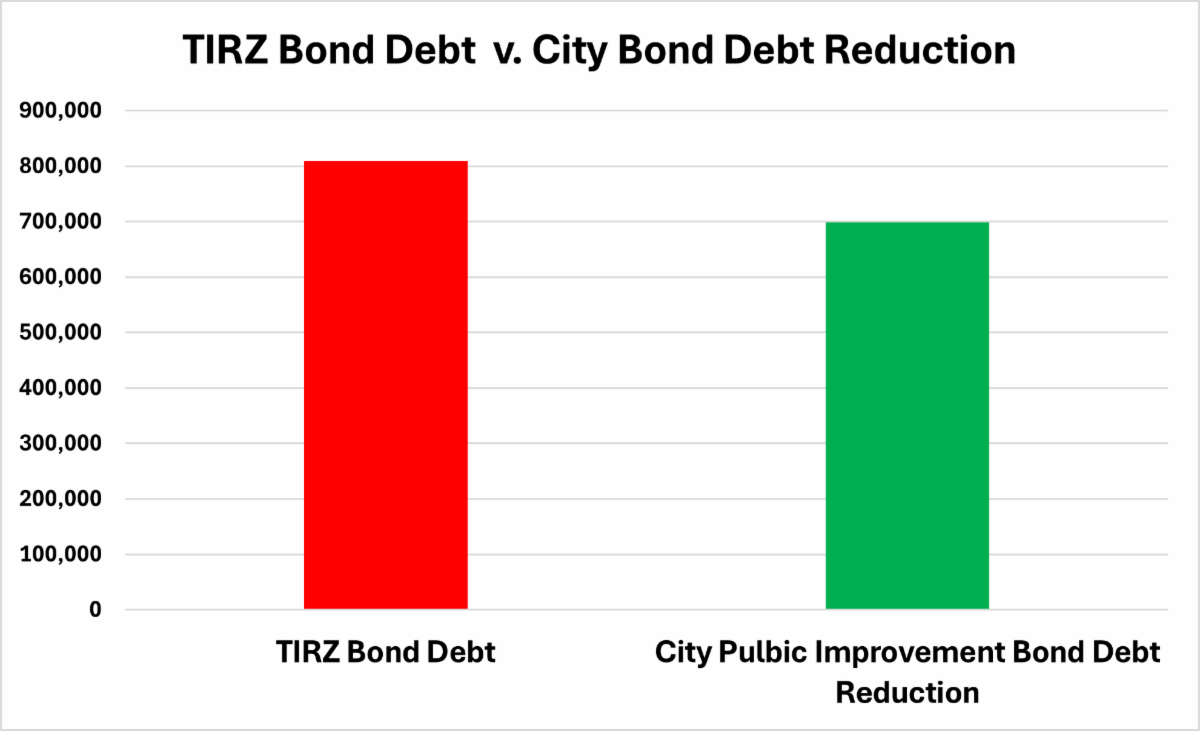

The TIRZ bonds also have provided a means for the City to sidestep the taxpayers’ decision to require pay-as-you-go financing for street and drainage improvements in the Renew Houston charter amendment. That charter amendment provided that the City would not issue any further bonds for street and drainage improvements, and as the bond debt was paid down, the savings in the debt service payments would go into the dedicated street and drainage fund.

As a result, over the last decade the City has reduced its public improvement bond debt by $700 million. But the paydown in debt from that initiative has now more than been replaced with TIRZ bonds, which must be ultimately serviced by the general fund, thus completely frustrating the voters’ dictate to the City.

The mountain of debt the TIRZs have run up is just one example of how opaque the finances of these entities are. Over a quarter of a billion dollars of Houstonians' tax dollars flows through these entities every year with minimal oversight by the City. If property values keep rising and the City Council keeps allowing the TIRZs to annex more properties and extend their terms, the portion of the City’s property taxes that are committed to this murky world of consultants, questionable expenditures, and some outright boondoggles and fraud, will only grow.

Note 1 – The City’s total consolidated bond debt is much higher at about $13 billion. However, the combined utility system (water-sewer system) and the Houston Airport System owe about three-quarters of that bond debt. That debt is repayable only from their revenues, not property taxes. The only other significant tranche of debt secured by property taxes is approximately $1.3 billion of pension bonds. See Annual Certified Financial Report, 2023, p. 258.