The accounting for the City of Houston finances is broken down into a number of discreet “funds.” For the most part, these funds are required by law to be segregated and only limited amounts may be transferred from one fund to another one. In some cases, the funds are actual separate legal entities, while others are “divisions” of the City, which various laws require their finances to be accounted for separately.

To make matters even more confusing, there are differences in how the finances are reported by the City in its monthly reports (MOFRs) and in its audits. For those of you with an accounting background, the difference between the two systems can generally be described as the difference between cash and accrual accounting. Both serve important functions, but they are very difficult for even a seasoned observer to reconcile. For the most part, I am going to be using numbers from the budget and monthly reports in my discussions, but there are some areas, like the pensions, where we will have to look at the accrual numbers.

There are literally dozens of different funds that comprise the City’s finances and the financial condition of the different funds varies dramatically. It is impossible to understand the City’s overall financial condition without understanding the role of these different and the looking at the financial dynamics of each.

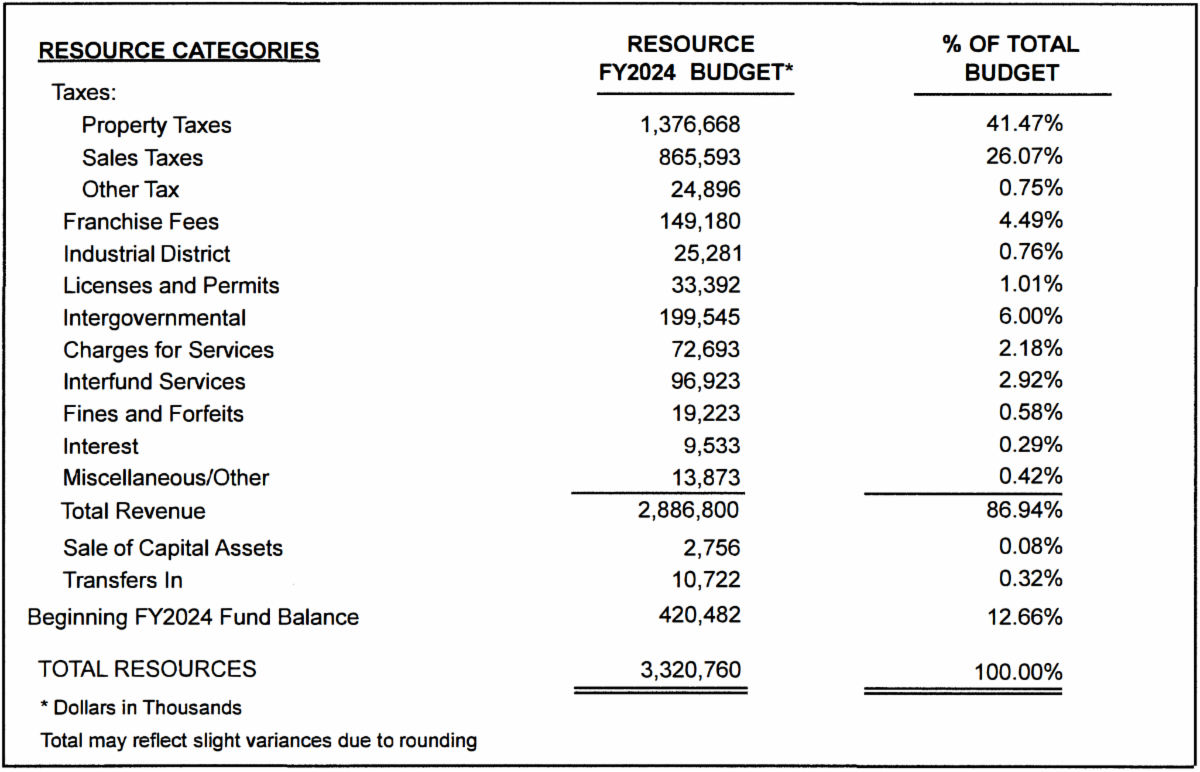

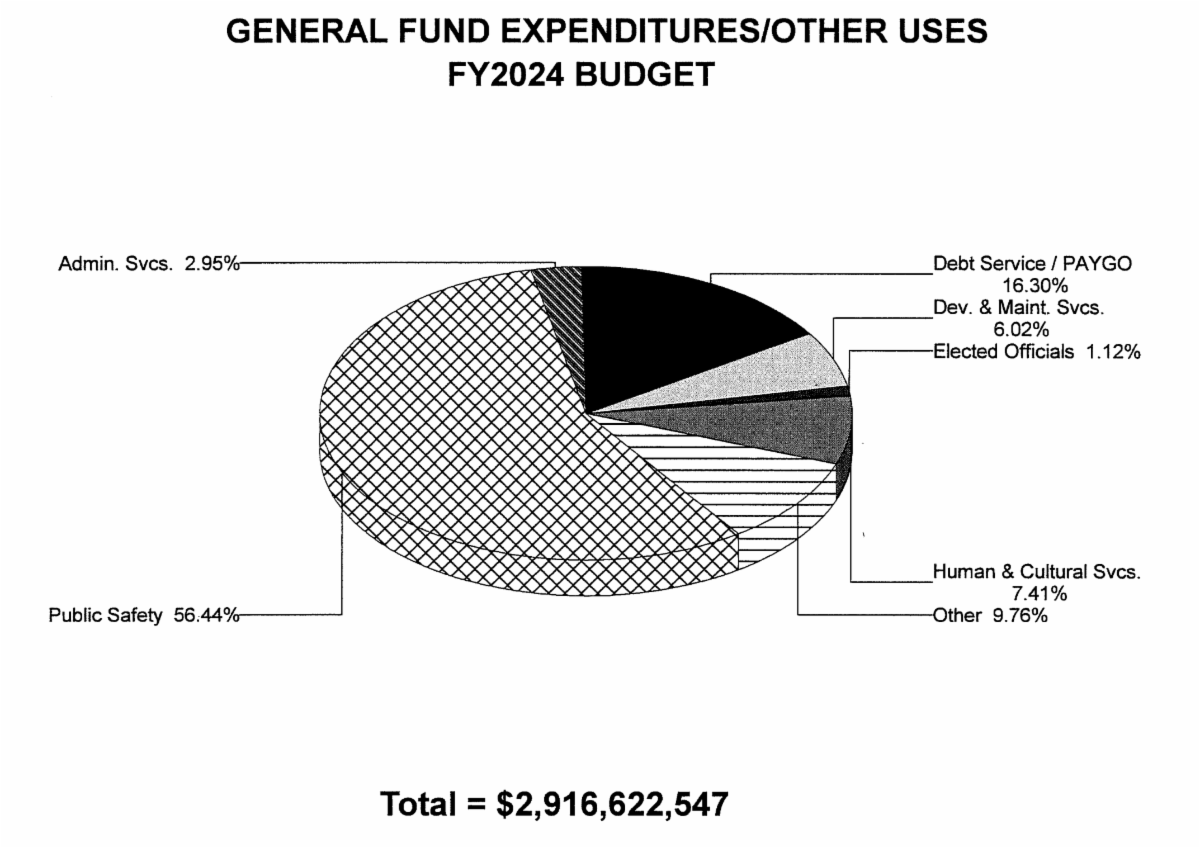

Today, I am going to devote my discussion to the General Fund. It is the largest fund, and it pays for most of our city services such as police, fire, most street and drainage work, parks, the health department, and the City’s administration. The budget for the General Fund this year is $2.9 billion. That was a 5% increase from the previous year.

The two largest revenue sources for the General Fund are property taxes (47%) and sales taxes (30%). Property taxes and sales taxes were projected to be up by 8.2% and 7.4%, respectively, this year.

The police and fire departments are 35% and 21% of General Fund expenditures, respectively. The next largest expenditures are debt service (12%) and transfers to the “dedicated drainage and street fund” (DDSF) (4%).1

The budget projects a small current deficit for the year of $1.3 million. According to the monthly reports through December (half the fiscal year, see p. 12), actual revenues and expenditures appear to be coming in fairly close to budget. However, to achieve that de minis deficit, the City is relying on $200 million in “intergovernmental transfers.” This is mostly left over COVID funding from the federal government. Without that funding, the General Fund would run a 7% deficit this year and burn through about half of the City’s current General Fund balance.

As you will see from my subsequent discussion of the other funds, the General Fund is where almost all of the City’s financial problems lie. According to the Mayor, the COVID funding will be exhausted by the end of next year. At the same time, he will be grappling with settling the firefighter’s pay dispute, coming up with more funding to fix streets, improve trash service, do a better job of maintaining our parks, adding police officers... the list goes on. In addition, with the City’s population growth stalling and inflation subsiding, the prospects for robust revenue growth are not promising.

Unraveling the mess he has inherited in the General Fund will be the biggest challenge Whitmire will face in his first term in office.